In an era of rapid solar adoption and surging demand for energy storage, supply chain vulnerabilities can make or break project timelines, profitability, and long-term reliability. US automakers like Tesla, General Motors, and Ford are accelerating domestic battery production to capitalize on Inflation Reduction Act (IRA) incentives and enhance supply security. Yet, upstream realities persist: China maintains dominant positions in critical mineral processing, LFP battery technology, and component manufacturing.

This guide equips solar installers, distributors, project developers, and energy storage procurers with a practical framework for building resilient solar + energy storage supply chains. True resilience means strategic diversification — not isolation from any single region — to balance policy incentives, cost efficiency, safety, and performance. Partners with proven global scale and LFP expertise, like Sunpal, help buyers achieve this balance effectively.

The Current Global Battery and Energy Storage Supply Chain Landscape

The global lithium-ion battery market surpassed USD 150 billion in 2025, reflecting over 20% year-over-year growth fueled by electric vehicles and stationary battery energy storage systems (BESS). China continues to manufacture well over 80% of global battery cells, with even stronger dominance in upstream segments.

China controls the vast majority of refining capacity for lithium, cobalt, and graphite, and holds over 98% of global LFP cathode active material production. LFP batteries now account for more than half of global EV battery deployments and over 90% of stationary storage applications worldwide, driven by their superior safety profile, longevity, and cost advantages — often 30–40% lower per kWh than NMC alternatives.

In the United States, the IRA has catalyzed significant localization efforts. Battery manufacturing capacity is expanding rapidly through gigafactories from Tesla, GM, Ford, and joint ventures with partners such as LG Energy Solution and Panasonic. Pipeline announcements suggest potential for over 1,000–1,200 GWh of capacity, primarily focused on cell assembly, module production, and system integration. Despite these advances, many upstream components — including precursors, cathode materials, and processed minerals — still rely on efficient global networks.

This hybrid reality is particularly relevant for the solar + energy storage sector. In 2025, the U.S. installed a record 57.6–58 GWh of new battery storage capacity, with strong growth in utility-scale, commercial & industrial (C&I), and residential segments. Texas and California together accounted for a large share, though deployments are diversifying to states like Arizona, Nevada, and New Mexico. NEM 3.0 in California has accelerated behind-the-meter solar + storage pairings, as reduced export credits push homeowners and businesses toward self-consumption and resilience.

1. Raw Mining

Lithium, Cobalt, Nickel, Graphite

Diversified global supply

LFP uses iron & phosphate2. Refining & Processing

Battery-grade lithium, graphite, precursors

Critical supply chain bottleneck

LFP Cathode >98%3. Cathode Materials

LFP, NMC, NCA production

20–40% cheaper than NMC

6000+ Cycles4. Components

Graphite Anode, Separator, BMS

Stable pairing with LFP

Thermal Stability5. Cell Manufacturing

Prismatic, Pouch, Cylindrical Cells

LFP dominates stationary ESS

>90% ESS Market6. Module & Pack

Battery Pack + BMS Integration

US/EU expansion via IRA

Local Assembly Trend7. Final ESS Integration

ESS + PCS + Inverter + EMS

Residential / C&I / Utility

10–15+ Years LifetimeFor solar installers and project developers, this landscape underscores an important truth: While “American-made” final assembly grows, access to high-performance, cost-effective LFP technology at scale remains heavily supported by established global capabilities. Understanding these dynamics allows procurers to make informed decisions that optimize both policy compliance and project economics.

Risks of Over-Reliance on Any Single Region

Relying too heavily on any one geographic area introduces substantial vulnerabilities. Geopolitical tensions, evolving tariffs, port disruptions, and raw material bottlenecks can cause months-long delays and significant cost overruns. Attempts at complete decoupling from mature supply networks would likely increase prices substantially while slowing the deployment pace required to meet renewable energy and grid stability targets.

Solar installers operating in dynamic markets such as California under NEM 3.0 or Texas's ERCOT-driven opportunities understand this acutely. Battery shortages directly translate into lost revenue from energy arbitrage, peak shaving, backup power services, and increased customer acquisition challenges. Nascent local supply chains, while strategically important, often face higher upfront costs and scaling hurdles that do not yet fully match the performance benchmarks of established LFP solutions in safety and cycle life.

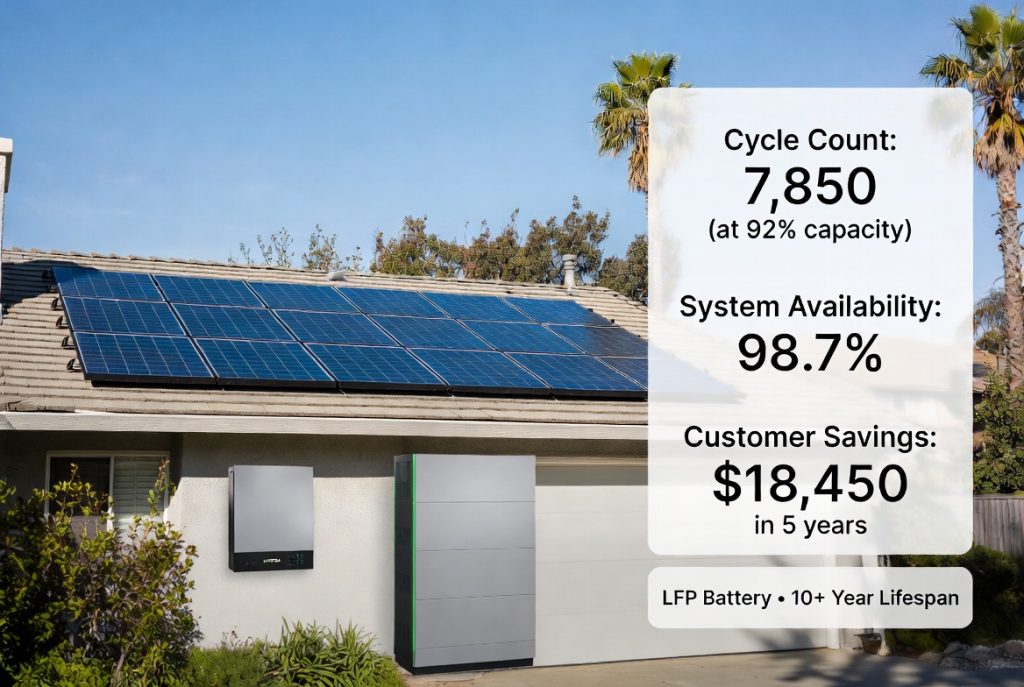

LFP chemistry stands out for stationary solar + storage applications. It delivers exceptional thermal stability with greatly reduced risk of thermal runaway, cycle lives frequently exceeding 6,000 cycles at 80% depth of discharge, and markedly lower total cost of ownership compared to NMC in most grid-tied and backup scenarios. These attributes make LFP the preferred choice for residential, C&I, and utility-scale projects where reliability and longevity drive long-term profitability.

| Parameter | LFP (LiFePO4) | NMC (Nickel Manganese Cobalt) | Winner & Notes (Solar + Storage) |

|---|---|---|---|

| Cycle Life |

4,000 – 10,000+ cycles Premium: 6,000–10,000+ High Durability

|

1,000 – 3,000 cycles Premium: up to 2,000–4,000 Moderate Life

|

LFP – Essential for daily cycling in solar + BESS applications (arbitrage, self-consumption). |

| Cost per kWh (2025) |

$70 – $100/kWh Avg: ~$81/kWh |

$110 – $130+/kWh Avg: ~$128/kWh |

LFP – 20–40% lower upfront cost and significantly better lifecycle economics. |

| Safety / Thermal Stability |

Superior safety Thermal runaway ~270–300°C Lower oxygen release |

Moderate safety Thermal runaway 150–210°C Higher oxygen release |

LFP – Much safer for residential, C&I, and utility-scale ESS (no cobalt/nickel toxicity). |

| Energy Density |

90 – 160 Wh/kg (pack: ~120–180 Wh/kg) |

150 – 280 Wh/kg (higher by 20–50%) |

NMC – Advantage for EVs; less relevant for stationary storage. |

| Service Life |

10 – 15+ years Low degradation |

6 – 10 years 5–8 years in daily cycling |

LFP – Longer lifespan reduces replacement frequency and project risk. |

| Round-Trip Efficiency | 92–96% | 94–97% | Slight edge NMC – but difference is negligible in solar applications. |

| Operating Temperature |

Wider range Better high-temp stability |

Narrower range | LFP – More robust in harsh or variable climates. |

| Lifetime TCO |

30–40% lower overall cost Fewer replacements |

Higher due to shorter lifespan | LFP – Clear long-term economic advantage. |

| Best Applications |

Solar + BESS Residential / C&I / Utility storage |

EVs, aviation, mobile high-density systems | LFP dominates >90% of stationary energy storage deployments globally. |

• LFP dominates stationary energy storage due to safety, long cycle life, and lower cost structure.

• NMC retains advantages in energy density for EV applications, not for stationary BESS.

• Even with slightly lower energy density, LFP achieves significantly better total cost of ownership (TCO).

Market context: LFP now accounts for >90% of new stationary storage deployments in many global markets.

Over-reliance on emerging domestic-only supply also risks project delays amid rapid demand growth. A diversified approach mitigates these risks while capturing the best available technology and economics.

Core Principles of Supply Chain Resilience in Solar + Energy Storage

Effective resilience is built on five foundational principles:

- Strategic Diversification — Develop multi-supplier and multi-regional models that leverage global strengths rather than pursuing unrealistic full isolation.

- Technology-First Selection — Prioritize LFP for stationary storage due to unmatched safety, cycle life, and cost structure in solar + BESS applications.

- Traceability and Quality Assurance — Require full transparency in material sourcing paired with internationally recognized certifications such as UL, IEC, and UN38.3.

- Policy Navigation — Design hybrid sourcing strategies that maximize IRA tax credits and ITC incentives while ensuring compliance and cost competitiveness.

- TCO Optimization — Focus on lifetime value metrics including degradation rates, maintenance needs, warranty support, and round-trip efficiency instead of initial purchase price alone.

Additional practical elements include strategic inventory buffering, multi-year framework agreements with reliable partners, regional warehousing to reduce lead times, and robust contingency planning. Real-time supply tracking tools and periodic supplier audits further strengthen the chain.

For solar companies serving North American markets, these principles translate into faster project delivery, more competitive bids, and higher customer satisfaction through reliable long-term performance. Partners who maintain strong upstream relationships and invest in North American technical support and pre-stocking programs offer a clear advantage in today's environment.

Practical Procurement Strategy Framework: A Step-by-Step Guide

Step 1: Define Clear Project Requirements

Begin with a detailed assessment of energy capacity needs, discharge duration, safety priorities, expected cycle frequency, local policy incentives (IRA, ITC, state-specific rebates), and site-specific constraints. For the majority of solar-paired storage installations, LFP emerges as the optimal chemistry due to its safety and longevity profile.

Step 2: Map the Full Supply Chain

Identify potential vulnerabilities across cells, battery management systems (BMS), inverters, enclosure assembly, and logistics. Distinguish between areas where global scale drives efficiency (e.g., cell manufacturing and cathode materials) and where local value-add enhances compliance or speed (final system integration and installation support).

Step 3: Evaluate Suppliers Using a Resilience Scorecard

Score potential partners on: manufacturing scale and vertical integration depth; proven global delivery track record; financial stability; certification portfolio; North America-specific support capabilities (technical service, local inventory, warranty execution); and transparency regarding materials and performance data.

Step 4: Build Hybrid Sourcing Models

Combine high-quality global LFP cells from established leaders with regional assembly, integration, and value-added services. This model delivers systems that align with IRA objectives while remaining highly competitive on price and performance. Many successful U.S. solar + storage projects already utilize this approach to balance incentives with economics.

Step 5: Establish Ongoing Monitoring and Adaptation

Implement supplier performance dashboards, contingency suppliers, and regular audits. Build strong collaborative relationships with partners who maintain North American inventory, offer rapid technical response, and provide clear documentation for incentive compliance.

| Metric | Quality LFP System (High-Volume) | NMC / Alternative System | Advantage & Interpretation |

|---|---|---|---|

| System Size | 10 kWh Residential / Small C&I | 10 kWh | Baseline comparison |

| Upfront Cost (Installed) | $9,000 – $12,000 Lower Capex |

$11,000 – $14,000 Higher Capex |

LFP: 15–25% lower initial investment (inverter + BMS included) |

| Net Cost after 30% ITC | $6,300 – $8,400 | $7,700 – $9,800 | LFP remains ~15–20% cheaper after incentives (IRA) |

| Cycle Life | 6,000 – 10,000+ cycles High Durability |

2,000 – 4,000 cycles Lower Longevity |

LFP: 2–3× longer lifecycle → major replacement savings |

| Expected Service Life | 12 – 15+ years | 7 – 10 years | LFP: +4–6 years operational advantage |

| Annual Savings | $1,200 – $1,800 | $1,100 – $1,600 | Slight LFP edge due to higher usable cycles |

| Replacement Frequency (15 yrs) | 0–1 replacements | 1–2 replacements | LFP significantly reduces downtime & labor cost |

| Total Lifecycle Cost (15 yrs) | $18,000 – $24,000 | $26,000 – $35,000 | LFP: 25–35% lower total ownership cost |

| Payback Period | 4.2 – 6.5 years | 5.8 – 9.0 years | LFP: 20–30% faster payback (1.5–2.5 years earlier) |

| LCOS (Levelized Cost of Storage) | $0.08 – $0.12 / kWh | $0.13 – $0.19 / kWh | LFP: 30–40% lower cost per delivered kWh |

| Maintenance Cost | $150 – $300 / year | $250 – $450 / year | LFP: Better thermal stability reduces O&M expenses |

Data Sources: BloombergNEF (2025 battery & storage outlook), Benchmark Mineral Intelligence, BSLBatt, GSL Energy, Sunlith Energy, and US residential/commercial installation benchmarks (2025–2026).

This framework helps solar installers and developers reduce risk, improve margins, and deliver superior value to end customers in competitive markets.

Real-World Case Studies and Best Practices

U.S. solar installers have successfully deployed hybrid-sourced LFP storage systems across California, Texas, Arizona, and other states. These projects consistently demonstrate high availability (often exceeding 95%), excellent round-trip efficiency, and seamless integration with existing solar PV arrays under demanding grid conditions.

In California, NEM 3.0-driven residential and C&I installations frequently pair solar with LFP batteries to maximize self-consumption and provide reliable backup during outages. Texas projects leverage storage for ERCOT arbitrage and grid support, benefiting from rapid deployment enabled by stable global cell supply paired with local integration.

Utility-scale examples show LFP-based BESS delivering grid stabilization services with outstanding uptime. Lessons from the automotive sector — where major manufacturers maintain global partnerships while expanding domestic capacity — apply directly to solar + storage. The most successful procurers treat supply chain strategy as a competitive advantage rather than a compliance checkbox.

Why Partnering with Proven Leaders Strengthens Resilience

Experienced global manufacturers with deep LFP expertise, such as Sunpal, provide a strategic advantage by combining technology leadership, rigorous quality systems, comprehensive certifications, and reliable delivery at scale. These attributes complement ongoing U.S. localization efforts rather than competing with them.

Sunpal's LFP solutions emphasize 6,000+ cycle performance, exceptional safety characteristics, and strong cost-effectiveness — aligning with the global standard for solar + storage applications. North America-oriented services, including technical support, pre-positioned inventory, and clear understanding of IRA requirements, help installers and distributors minimize risks while maximizing project profitability.

By partnering with organizations that maintain transparent, robust supply relationships and invest in customer success programs, buyers gain stability, predictable pricing, and the ability to scale deployments quickly in high-growth markets.

Conclusion and Actionable Next Steps

Building a solar + energy storage procurement strategy resilient to single-region risks requires thoughtful diversification, a focus on LFP technology, and collaboration with capable global partners. While U.S. manufacturing momentum accelerates in downstream assembly, established strengths in processing and LFP innovation continue to serve as valuable assets for industry-wide growth. Global competition paired with cooperation will keep driving innovation and cost reductions.

Explore Sunpal's LiFePO4 Battery and Solar Energy Storage Solutions — engineered for performance, safety, and long-term supply resilience.

🧠 Schedule Consultation

Speak with a North America energy storage specialist to evaluate system design, supplier strategy, and IRA optimization.

Book Consultation